Posted by Marc Hodak on April 3, 2016 under Governance, Regulation without regulators |

Regulators are finally looking at unicorns–private companies grown to over $1B–and all they see are unbridled horses. SEC Chairwoman Mary Jo White is bothered:

White echoed the concerns of some industry insiders that these tech start-ups are missing out on the market discipline public companies receive by being accountable to the whims of public shareholder. (sic)

And on top of losing out on the whimsy, White adds:

For these companies to be successful, investors must be confident that they are being treated fairly and that companies are being transparent.

That these things were written without irony shows how unmoored our discussion of corporate governance has gotten from reality. Clearly, the poor investors of Uber, Airbnb, and Snapchat must be slapping their foreheads, saying “THAT’s why success has eluded us! We need more SEC oversight!”

I’m sure the good governance mafia (GGM) will accuse me of being tone deaf with regards to the benefits of greater SEC oversight of these giant, private firms. Clearly I don’t get that without an additional two thousand pages of rules, these companies would just do whatever they want, and their shareholders would suffer. Because cheating your shareholders is how you build great businesses.

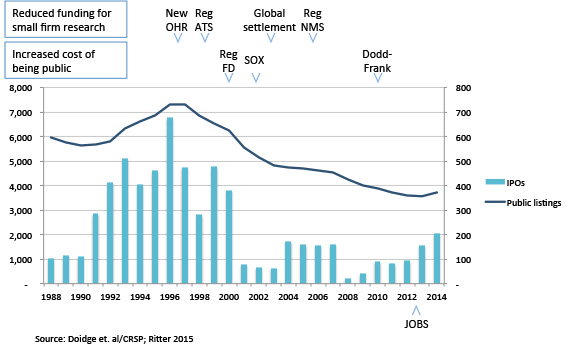

Here is an alternative view, one I recently shared at a major economic forum:

This chart shows some of the regulations that have multiplied the costs of being a public company over the last couple of decades. Yes, it’s possible that something other than these escalating public company costs led to the collapse of the IPO market. It’s possible that something other than these escalating public company costs have contributed to the dramatic decline in public companies. You have endogenous factors, omitted variables, and all that stuff. I understand.

But people who inhabit the executive suites, board rooms, and trading floors don’t need this chart to tell you what happened, especially those who grew up in the ’80s and ’90s when “going public” was the epitome of success. They will tell you that the costs of being public now outweigh the benefits for all but the largest firms. They know that a bad cost-benefit trade-off is not good for shareholders, regardless of what self-appointed “shareholder advocates” might say.

Admittedly, this all sucks for the average retail investor. Those without the net worth to be allowed to invest in private equity or venture capital opportunities are now cut out of a fast growing, lucrative market. Many of these same retail investors belong to public or union pension funds that have agitated for this two-tiered capital market, where the rich have more choices than average workers.

The SEC has long left sophisticated investors alone precisely because they need the least protection. The private companies that have these investors on their boards are presumed to be adequately governed. Yet we now have a top regulator telling some of the winningest companies on earth that they are losers for not joining her club.

Posted by Marc Hodak on December 15, 2013 under Governance, Regulation without regulators |

Aubrey McClendon, former CEO of Chesapeake Energy Corp. (which, as far as I know had nothing to do with the bay near where I grew up), is pulling in billions in new capital via his American Energy Capital Partners LP. The partnership will have some unusual governance features:

American Energy Capital also disclosed a range of potential conflicts of interest. The sponsors can favor their own interests over those of investors. In addition, the partnership may invest in oil and gas properties where Mr. McClendon’s firm has interests. Mr. McClendon’s management group won’t owe a fiduciary duty to the partnership, according to its registration statement.

Now, would I buy into a partnership with such conflicts? Probably not.

Would I prohibit anyone else from buying into such conflicts? Definitely not.

This partnership may or may not prove to be as good a deal for its investors as Chesapeake was for theirs. I would leave it to others to discern the bet they are making. But I would not prevent them from making their bet. And once they buy into this partnership, I would not favor the government forcing a change to the rules they bought into for the sake of “good governance.”

If all this makes sense to you, and I know it won’t to everyone, then you should be disturbed when public companies are forced to reform their governance through a federalization of corporate rules that supersede their charters. We can’t know that such “reform” will enhance the returns of outside shareholders; no governance regulation adopted by Congress over the last couple of decades had any empirical support that it would actually help shareholders, either before it was adopted or after it was implemented. But we do know that the reforms will cost every company in three ways:

(1) The Compliance CAFE (Corporate Advisers Full Employment)

(2) The occasional cost of sub-optimal decisions because of decision-making constraints created by the rules, i.e., unintended consequences

(3) The costs of lawsuits alleging a breach of the rules, regardless of their actual breach, because it is often less expensive to settle these suits than to fight them and win, i.e., the Plaintiff Lawyer’s Tax

This is not to say that we shouldn’t have any rules with regards to corporate governance. But I would suggest that the rules agreed upon by the original parties to the transaction should be given much more of the benefit of the doubt than those dreamed up by a meddling Congress. Even bad bets contribute to our progress.

Posted by Marc Hodak on July 7, 2010 under Regulation without regulators |

The WSJ comes up with a story about a novel idea;

Even before a financial-regulatory overhaul takes effect, some big investors are imposing their own rules on risk.

Several public and corporate pension funds are curtailing or revisiting their use of derivatives out of concern for hidden risks they may carry. In Oklahoma, a public pension fund replaced Pacific Investment Management Co., led by well-known investor William Gross, as one of its bond-fund managers, citing the risks of its use of derivatives whose values couldn’t be cross-checked in audits.

In other words, big investors are actually looking for ways to account for risk as well as returns in their investing strategy–without the government forcing them to do it!

For those of us with finance training, which you’d think any major fund could afford and would consider a prerequisite to opening their doors, accounting for risk seems like a logical step rather than a great leap. Reviewing one’s risk management in the aftermath of a financial crisis would seem like something your parents wouldn’t need to remind you about. If the Okies don’t understand what Bill Gross is doing, they should get out of his fund (or hire a Wharton grad who gets this stuff, or both).

In my mind, the real headline would be, “Major investment fund does not change its M.O. after financial crisis.” The would be the story of the only two financial firms not affected by the pending financial reform bill.

Posted by Marc Hodak on February 3, 2010 under Invisible trade-offs, Regulation without regulators |

So, Toyota, builder of one of the most dependable machines in history, is being pummeled in the press for a quality problem that can’t quite be isolated. The U.S. government, which is constitutionally incapable of keeping its nose out of other people’s business, is not content to let the horror of bad publicity and Toyota’s legendary engineering do the job of righting things–the politicians have to pile on:

“This is very serious,” (Transportation Secretary) LaHood said at a breakfast with reporters in Washington. “After I talk with (Toyota’s CEO), they’ll get it. We’re going to keep the pressure on.”

Mr. LaHood said Transportation Department officials flew to Japan in December to meet with Toyota executives and remind the company “about its legal obligations.” The agency, he said, “followed up with a meeting at DOT headquarters in January to insist they address the accelerator pedal issue.”

Because, if the senior U.S. transportation bureaucrat didn’t tell them to do it, Toyota would gladly continue allowing the quality issue to fester, destroying seven decades of branding as the highest quality car manufacturer in the world, and killing off customers as an added bonus.

But there is, no doubt, more to this spectacle than meets the eye.

Read more of this article »

Posted by Marc Hodak on September 1, 2009 under Regulation without regulators |

SEC Chairman Mary Schpiro sees Wall Street’s aggressive pursuit of top brokers, and sees red:

“Certain forms of potential compensation may carry with them enhanced risks to customers,” Schapiro wrote. “For example, if a registered representative is aware that he or she will receive enhanced compensation for hitting increased commission targets, the registered representative could be motivated to churn customer accounts, recommend unsuitable investment products or otherwise engage in activity that generates commission revenue but is not in investors’ interest.”

This sounds good…to people unfamiliar with the way the average owner balances incentives and controls. If all we had to worry about were incentive effects, then the average restaurant owner who allowed their waitresses to keep their tips would risk their waitresses nudging their customers toward the more expensive fares like the unpriced specials. The average law firm billing their lawyers by the hour would risk their associates padding their hours to the detriment of their clients. The average district attorney’s office whose DA’s election chances are increased by headlines might pursue headlines at the expense of justice in the case of politically unpopular individuals.

These things all happen, of course, but that’s not the point. The point is that it is impossible to disentangle the sensible from the perverse aspect of common incentives. Allowing a waitress to keep her tips encourages better service. Allowing lawyers to bill by the hour encourages them to go the extra mile to dig up the materials that will help their clients win their cases. Requiring DAs to go up for election provides a measure of accountability to the public the DA is supposed to serve. Similarly, giving brokers an interest in the commissions they generate can encourage them to seek out new customers and recommend suitable investment products that they are selling to a largely skeptical public.

What’s missing from Shapiro’s analysis is the fact that incentives aren’t implemented in a vacuum. They are implemented alongside controls. The waitress who somehow snookers her customers, even if they don’t know they’ve been snookered, is liable to be chastised by her boss if he cares about the reputation of his business. The partners are supposed to monitor the reputation of their firm. The governor and the press are supposed to monitor the DA. Are there monitoring failures? Of course. But that’s not an indictment of the incentives, either.

Read more of this article »

Posted by Marc Hodak on July 1, 2009 under Collectivist instinct, Regulation without regulators |

In this case, though, I appear to be in good company:

The standard competitive market model just doesn’t work for health care: adverse selection and moral hazard are so central to the enterprise that nobody, nobody expects free-market principles to be enough.

Whenever I see such nonsense, I have to keep reminding myself that the trade theories for which Krugman won his Nobel Prize were explanatory and predictive. Krugman did not win a prize for mechanism design; he could not have predicted E-bay.

The idea of people bidding for stuff they can’t really see from people that they’ve never met is fraught with asymmetrical information. Honest sellers could not hope to compete with liars selling competitive products. Honest bidders could not hope to compete with fraudulent bids that may not be honored. Such a market, failing as it does the test of a “standard competitive market model” could never exist.

Except that it does.

Read more of this article »

Posted by Marc Hodak on April 3, 2008 under Regulation without regulators |

I just got back from my annual teaching visit in Switzerland. I left for Zurich earlier this week, soon after finishing an article I had written for Forbes about the governance challenge of ‘utopia.’ I wasn’t thinking about Switzerland when I wrote the article, but I was thinking about the article soon after I arrived there. One of my points in the article (hopefully coming out soon) was that it’s dangerous to invest utopian hopes in any particular leader; if they don’t disappoint you during their reigns, you will surely be disappointed by their successors. This is a useful lesson to remember during our frenetic presidential campaign, where it seems everyone is looking for a hero or a savior, and the candidates seem happy to play the part.

While riding a quiet train past Swiss villages, the titular question came to mind. I would guess that most people who read this, and others like you, can name the British Prime Minister, French President, and German Chancellor. But no one knows the president of Switzerland. To be sure, the heads of the larger European countries are very powerful individuals, and their nations have far more vigorous foreign policies, which keeps the names of their leaders in the press with some frequency. That’s my point.

Switzerland is among the most peaceful and prosperous nations on earth. But I’ve never heard of any Swiss president, let alone one leading this or that crusade. It seems to me that there is a relationship between those facts.

Posted by Marc Hodak on December 12, 2007 under Regulation without regulators |

One of my alert students, after a discussion of informal (e.g., market-based) regulation versus formal (e.g., government) regulation in class last night provided this video by leftist animator Mark Fiore:

If I were of Fiore’s ilk, I would probably object that animators should not be allowed to produce socio-political commentary without a basic education in political science and economics, using this video as an example of how dangerous that would be.

Alas, since I believe in freedom, all I can do is shake my head that people might actually believe that problems with meat or toys or mine safety are actually the result of too little government regulation.

In fact, despite voluminous government regulations that actually exist in nearly all markets, the most potent regulations remain the informal type. To understand the depth and power of informal regulation, one can begin by looking at the incentives of the players involved. Why would a regulator in Washington have more of an interest in Mattel’s product safety than Mattel’s managers or investors? How did Mattel’s shareholders or managers come out ahead after this summer’s string of recalls? It’s hard to imagine that anyone has a greater interest in not harming Mattel’s customers than Mattel itself, especially for a large company where any scandal in even the smallest area of their business affects their brand across all their businesses.

Then, one must consider the responsiveness to particular scandals. In a CNN article about the third of Mattel’s recalls, they included the government’s reaction in the middle of the article, and the market’s reaction at the very end. It’s kind of a Rorschach test of one’s view of the world to select which statement gives you the most comfort:

“The CPSC has its own investigations currently underway to make sure products on shelves are meeting US safety standards,” said (Julie) Vallese (CPSC Director of Information)

Wal-Mart has also hired independent laboratories to carry out 200 tests a day, focusing first on toys made for children up to the age of three, it said.

I don’t know what got us to the point where most people seem to believe that any failure in the marketplace is the product of market failure, correctable by government regulation. Somehow, people leave school with the premise that businessmen are indifferent to harming their customers, that the leaders of the largest businesses are the most remote and indifferent, that their reputations have no value to them, and that only government officials have the unerring care, foresight, and capabilities to to actually protect consumers.

Posted by Marc Hodak on October 16, 2007 under Regulation without regulators |

For my Canadian readers, you can check me out on B1 of your Globe and Mail. The author did a good job of representing me. She may have slightly overstated things to say that my “consulting business (is) based mainly on applying mechanism design theory,” (it’s more broadly about using incentives to minimize agency costs and improve decision making), but frankly I don’t know of anyone who incorporates mechanism design theory into actual, internal corporate practices to the extent I do. The author seemed thrilled, in fact, to find someone who actually applied this theory to real life business problems rather than another professor to provide theoretical solutions to hypothetical problems.

Alex Tabarrok did an excellent job illustrating the basic concept of mechanism design theory. The author mentioned two of my business applications (executive incentives and corporate investment decisions), but those are fairly complex, and reading what Alex wrote inspired me to think of a simpler example of an application I’ve implemented. So, here is one:

I some situations, one manager has to transfer an asset (say, real estate) to a particular other manager. There is no possibility of competing buyers or sellers. Manager A must sell it to Manager B. At what price? A simple negotiation would quickly break down. The seller would ask for too much; the buyer would offer for too little; neither side has an incentive to provide an honest valuation. Agreeing to split the difference wouldn’t help–in fact, it would simply polarize the bid and ask prices.

So I overlaid an additional rule to this negotiation. I said that if the two managers couldn’t agree on the price, we would set aside their respective best and final offers, and go to a third party appraiser with some experience with that asset (real estate, in this example) and provide an estimated value. The appraiser wouldn’t even see the offers. We would then open up the best and final offers of the two managers, and the offer closest to the appraised value got their price. Think about how the dynamics are changed with this rule, and why the managers, in fact, were generally able to quickly come to agreement, almost never needing an appraiser to actually get involved.

I didn’t mention to the reporter the fact that I was also a professor.

Posted by Marc Hodak on July 25, 2007 under Regulation without regulators |

MySpace recently booted about 29,000 sexual predators from its site. Nobody asked them to do it. They just figured that it was good business to keep their young customers from getting, you know, raped. On the one hand, one could read that as a positive indicator that a private company has every incentive to police its space and keep it safe for its intended users. On the other hand, one can read that as the perfect excuse for government involvement in the Internet.

“The exploding epidemic of sex offender profiles on MySpace – 29,000 and counting – screams for action,” said Connecticut Attorney General Richard Blumenthal.

In North Carolina, Attorney General Roy Cooper wants a state law that would require children to obtain parental permission before creating profiles on sites such as MySpace, and require the site to check parents’ identity.

I guess that making MySpace the North Carolina AG’s deputy nanny can allow him to pretend to care more about my kids than I do. (I read the news, too, Roy.) I guess, too, that the action by MySpace doesn’t count as “action” as defined by the Connecticut AG. Politicians live by the premise that there is no regulation until the government does it, and voters will tend to believe them. Especially when it comes to protecting the children.

{kind=link}

{kind=link}

{kind=link}

{kind=link}