The unanticipated death of a public company top executive can often create an observable market reaction. Sometimes, this reaction is not flattering, as when the stock price jumps five to seven percent when a CEO dies because there was no other way for the shareholders to get rid of him.

On the other hand, you get examples of what happened when the market was hit with news that Ed Gilligan, American Express President and heir apparent to the CEO, passed away suddenly on Friday. Amex stock dropped about ten cents per share (after accounting for changes in the market overall)—a drop of about $100 million dollars. Which answers the question posed in this title: Yes, some people are clearly worth to their shareholders what they are being paid.

Ironically, this financial hit was the result of good governance. Amex did what it was supposed to do in clearly identifying a likely successor in case they should suddenly lose their CEO, as well as pave the way for his retirement. The value of clarity about successorship is supported by empirical evidence. So, in a sense, what Amex has lost in a worthy successor, besides whatever else Gilligan uniquely provided to the company, was simply giving back what they had previously gained from doing the right thing in establishing a clear heir to CEO Kenneth Chenault.

And now Chenault, who just lost a close colleague for whom he clearly had great affection, must once again groom another successor.

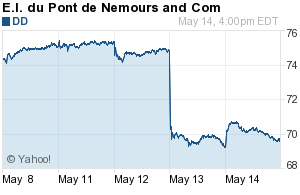

Those who have followed the Dupont/Trian contest know that the shareholders voted (barely) to retain the incumbent board. But two other, fascinating pieces of information are apparent from the aftermath of that vote regarding the investors’ reaction:

1. The market was surprised

2. The market was disappointed

A seven percent drop in the stock price is huge. Shareholders were clearly invested, so to speak, in seeing Trian win, even as they voted them down. So, while shareholders-as-voters accepted CEO Ellen Kullman’s explanation that Nelson Peltz does not know as well as she what is best for their company, shareholders-as-traders said, “Whoa, that was a terrible decision!” We assume that, being the same people, each making their judgments based on their individual, independent estimation about the future prospects of the company, and with the “wisdom of crowds” sorting out their discordant judgments into a useful, single verdict, we should see less schizoid outcomes.

Alas, this “crowd” effect works via very different mechanisms in proxy voting versus in market pricing. So, which result should management heed? Read more of this article »

[Professor] Barankay [of Wharton] randomly divided workers into two groups — a control group receiving no ranking and a treatment group receiving feedback with a ranking. He then sent an e-mail to all of the workers inviting them to return to do more assignments. The content of all the e-mails was the same, except that individuals in the treatment group found out how they ranked in terms of their answers’ accuracy. The aim was to determine whether giving people feedback affected their desire to do more work, as well as the quantity and quality of their work. Of the workers in the control group, 66% came back for more work, compared with 42% in the treatment group. The members of the treatment group who returned were also 22% less productive than the control group.

Prof. Barankay also offered workers either a job where they would be ranked or one where they wouldn’t be.

[T]he job without the feedback attracted more workers — 254, compared with 76 for the job with feedback.

“This was a surprising outcome, but it speaks to the paradigm of revealed preferences,” he notes. “Economists are usually very skeptical about what people say they will do. We focus on what people actually choose to do. Their choices convey information about what they care about. In this case, it seems that people would rather not know how they rank compared to others, even though when we surveyed these workers after the experiment, 74% said they wanted feedback about their rank.”

So, people generally don’t like to be ranked against their peers, even though they say they do, and rankings appear to encourage the high performers to slack off and the poor performers to give up. Contrary to theory, it also encourages high performers to leave and poor performers to stay. High performers are given the confidence to go out and find new challenges, while poor performers appear to get demoralized, and may have fewer options besides.

This research stands in contrast to research on tournaments, which appear to motivate more productive behavior. Thus, the research indicates that it depends on how the feedback and reward mechanisms interact. Competition can breed excellence, and competition includes comparisons and consequences. But comparison alone can breed complacency or demoralization.

CEO pay is generally discussed and debated from the point of view of more typical kinds of employees, from minimum wage teens to well-salaried executives, who work for what seem like arbitrary sums offered by frugal or venal owners, or their sometimes clueless representatives on the board. At this level of the discussion, one loses a key distinction about pay in a market economy, i.e., that one should be paid about what they’re worth. So, a relevant question in this debate that is never asked: What is a CEO worth?

Mark Hurd’s sudden, surprise resignation at HP offers a rare hint to the answer; in after-hours trading shortly after the announcement of his dismissal, HP’s stock declined by over 8 percent.

Ladies and gentlemen, that’s over $9 billion dollars in market cap.

So, while various pundits might claim that every CEO is replaceable, the question remains: at what cost? The answer isn’t found in the much vaunted proxy disclosures on executive compensation.

That $9 billion figure is a discounted future cash flow assessment of Mr. Hurd’s value. In other words, in the apolitical judgment of equity investors, the only people with the incentive to make this collective judgment correctly, the company would have been better off paying about $2 billion a year for the next five or six years to keep Mr. Hurd than to lose him.

In fairness to the board, the Mr. Hurd they let go, the man who broke the HP ethics code he had done so much to champion, was not quite the Mr. Hurd the investors thought they had before the Friday announcement. There was a legitimate concern that the expense-fudging Mr. Hurd could no longer govern with the same authority he had before this unfortunate news came out. But that’s not the point here.

The point is that the buttoned-down guy atop his Silicon Valley perch that HP’s investors thought they had was worth far more than the mere tens of millions that the media (check out the comments) and good governance types have regularly derided.

Confiscatory taxation: What is going on in Great Britain.

Contrast this with

Socialism: Using state power to penalize success and reward failure.

Using the threat of violence to take an extra $50,000 from someone making $1 million is not considered a crime if implemented by authorities elected by the people who are, for the most part, not being taxed at that level. In fact, these people call their confiscation the patriotic or moral thing to do. They will claim that most of the people being taxed are actually OK with it; but they don’t dare let the class of people paying it vote on whether they should all do so. They will claim that those who do not wish to pay it lose their claim to their money by virtue of their selfish desire to keep it; but they don’t see the irony of their preferences forcibly imposed on others as a baser form of selfishness, abetted as it is by coercion.

But the victims of this self-justified view of theft-disguised-as-patriotism-or-morality won’t sit still for the grasping hypocrisy. They will leave. They take their money and, more important, their wealth-creating talents, to friendlier climes.

New York State, in an obvious attempt to see just how much it can piss off its taxpayers, has sent an extraordinary notice to all its citizens. It warns them that not only will their tax rates be raised in 2009, but they will have to recalculate their 2008 taxes now based on the new 2009 tax rates in order to comply with the new law. I know you think you just misread that last statement, so read it again, and rest assured that it is correct.

Here’s how it works. Most income taxes need to be paid each quarter on an estimated basis; the state doesn’t want to wait until the end of the tax year to collect its loot. The typical rule for estimated taxes is the lower of either (a) 90% of your actual tax bill that you’ll eventually have to pay or (b) 100% of your last year’s actual tax bill. For most filers whose incomes are flat or growing, the easiest thing to do is to look at your tax bill for last year and just pay that in equal installments over the current tax year. Simple enough.

This year, New York is saying that if you wish to use the second option to pay estimated taxes, i.e., 100% of last year’s taxes paid, you need to recalculate the amount you would have owed last year based on this year’s higher tax rates.

That’s right, the lovely time you recently spent calculating your New York taxes, you need to go through that again now using the new tax rates so that the state can squeeze that last $100 from you without having to wait until next April. We really are talking about chickensh*t sums, here. For the 60% of people who hire accountants to do their taxes, the vast majority of them would ending paying more for this recalculation than they would owe in additional estimated payments.

Why would the state do such a crazy thing? Because the state’s politicians are desperate for those incremental dollars, and they truly don’t care if what it costs you to pay them the lawful amount.

Most debates on tax policy center on the elasticity of supply, i.e., the degree to which an increase in taxes will reduce the willingness of the person being taxed to continue engaging in the taxed behavior. For example, if raising the sales tax causes people to buy less such that the actual tax raised is minimal, and businesses will otherwise suffer from the reduced sales, most policy makers would say that’s not an efficient tax. In New York State, we now have proof positive that if a business has to pay someone doing no productive work $10,000 in order to get the state an extra $8,000, the politicians feel they are ahead. Such abuse of New York State taxpayers is why we are seeing more of this.

The unions have made a number of concessions to ensure the survival of Chrysler. The question now is what the company’s creditors will do… They have to look at the broad economic impact (of Chrysler collapsing) and not just their own short-term financial interest.

Representative Schauer understands what it takes to look beyond his short-term financial interest. He’s a community service kind of guy. Never worked at a productive job a day in his life. And just because 25 of the top 40 campaign contributors were unions (UAW was #8) doesn’t mean he’s serving his financial interests in arguing for the altruism of others. I don’t doubt this guy sincerely believes that stiffing the creditors will be good for the economy in a “broad impact” sort of way.

But if sacrifice is what this is really about, Congressman, please show us the way. I know a Chrysler bondholder, one of the “little guys” who hasn’t accepted government money. He voted for Obama, FWIW. He figures he can get about 65 cents on the dollar in bankruptcy, a little less on liquidation than restructuring. The politicians are asking them to take about 15 cents. My friend, hearing the Congressman from the UAW asking for some sacrifice, is willing to match him, dollar for dollar.

He says, “I’m willing to take my lumps to the tune of what I contractually signed up for, i.e., a 35 percent loss. I bought the bonds. I screwed up. If you, Mr. Congressman (or Senator Levin, or Governor Granholm, or any other of the politicians standing in front of your union masters and asking us bondholders for an additional sacrifice) are willing to look beyond your short-term financial interest, and share in my loss beyond what the market says I could get from bankruptcy, then I’ll do it.”

So, if you, Congressman Schauer, put up $30,000, my friend says he will take an additional $30,000 hit, below the 60 cents he currently expects. Put $100,000 into the Chrysler kitty, and he’ll put up $100,000. What do you say, Congressman? Senator? Governor?

I will pre-emtively and perhaps unfairly say, “I thought so. You’re happy to ask for sacrifice, as long as it’s coming from others.”

I’ll give my friend the last word:

There are people who have bought into these securities at already depressed prices. I’m not one of them. We picked them up at issuance. While the unions were happy to collect their well above-market wages and benefits, I watched the value of my bonds drop. Now that they’re willing to work for only slightly above market wages and benefits, they’re expecting me to suck up much worse losses.

He closed with an unprintable invitation for the politicians to engage in something that sounded like self-copulation.

Speak clearly directly into the mic, please. Now say again? At the moment you realized that your shareholders would be screwed by the ML transaction, and it was time to invoke ‘material adverse change’ to back out of it, why didn’t you do it?

I can’t recall if [Hank Paulson] said “we would remove the board and management if you [invoked the material adverse change clause to block the Merrill deal]” or if he said “we would do it if you intended to.” I don’t remember which one it was, before or after, and I said, “Hank, let’s deescalate this for a while. Let me talk to our board.”

There it is. When the BAC board, including Lewis, came face-to-face with doing right by their shareholders or keeping their jobs, they chose to “deescalate.” Later they rationalized: getting fired = systemic risk.

So, Ken, you decided not to back out of the deal, what about at least telling your shareholders what you were getting them into?

Q: Were you instructed not to tell your shareholders what the transaction was going to be?

A: I was instructed that ‘We do not want a public disclosure.’

Q: Who said that to you?

A: Paulson…

Q: Had it been up to you would you [have] made the disclosure?

A: It wasn’t up to me.

So, the government ordered you to shoot your shareholders from behind a curtain, and you pulled the trigger.